The Question Almost Every San Carlos Buyer Asks

Whenever someone starts thinking seriously about a real estate move in San Carlos, the same question comes up: "Should I wait for rates to drop?"

It is a reasonable question. Rates feel high, headlines push the idea that relief is around the corner, and waiting feels safer than committing. But "feels safer" and "is safer" are very different things, especially in a market like ours.

I pulled 15 years of MLS data on San Carlos single-family home sales to see what waiting has actually cost buyers historically. The answer is a lot more expensive than most people realize.

What Waiting Looks Like in San Carlos

Every 6-month delay on a $2.5M home in San Carlos has historically cost buyers across two fronts at the same time.

The first is appreciation. San Carlos has averaged roughly 8% annual price growth per MLS data going back to 2011, which translates to $50K to $150K in lost equity for every six months a buyer sits out the market.

The second is rent. For buyers currently renting, a typical San Carlos rental runs $5K to $7K+ per month. Over six months, that's another $30K to $42K gone, with nothing to show for it on the back end.

Add it up, and the total opportunity cost of a six-month wait sits between $80K and $190K.

The 15-Year Picture: What Being IN the Market Actually Looks Like

The case for waiting tends to lean on the idea that the market might pull back. The data does not support that hope in San Carlos.

San Carlos home values have compounded through:

- The 2020 pandemic rate spike

- The 2022 correction

- The high-rate environment of 2023 through 2024

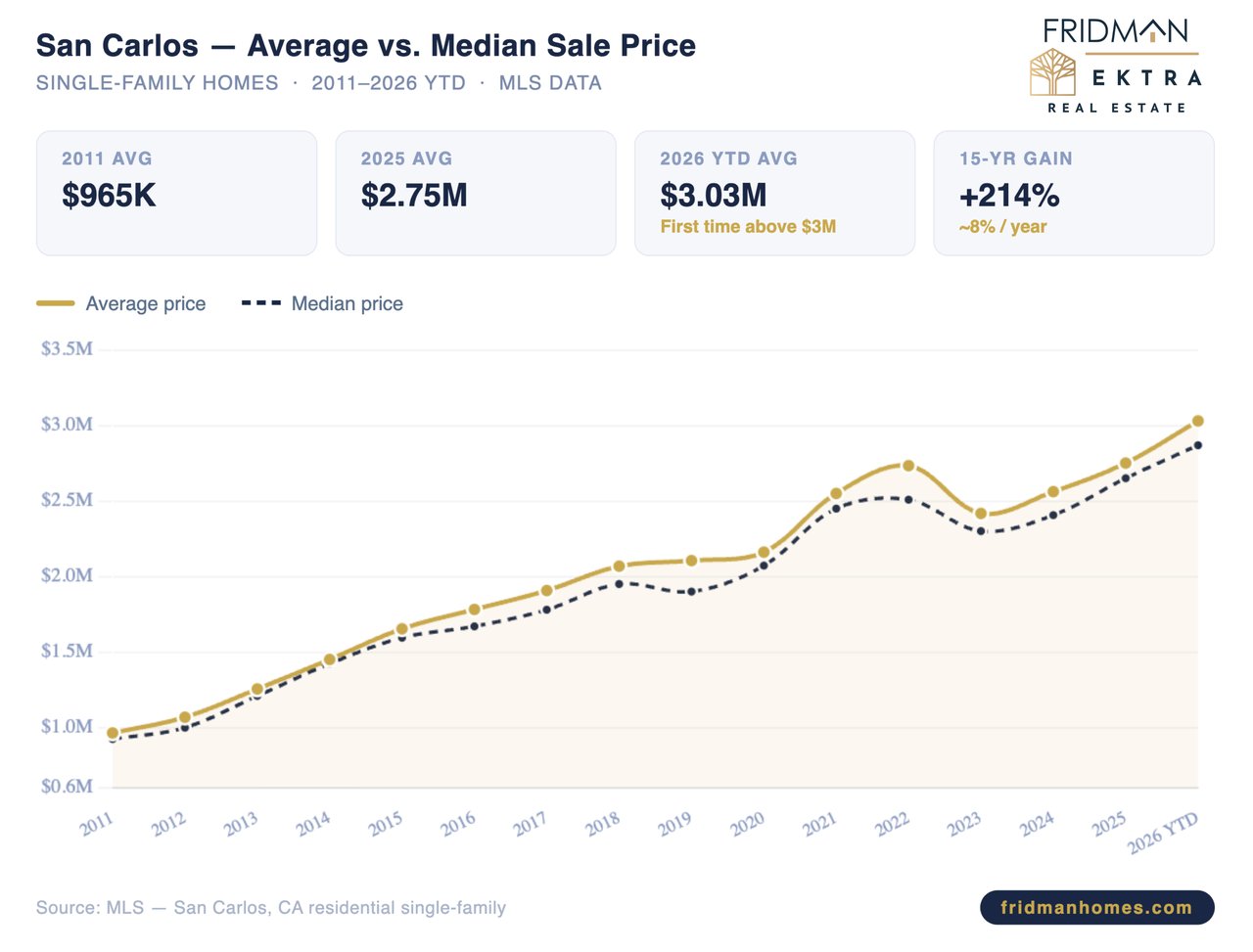

Every "bad time to buy" in the last 15 years still outperformed the waiting strategy, on average. According to MLS data, the average San Carlos single-family sale price went from $965K in 2011 to $3.03M so far in 2026, a 214% increase over 15 years.

That's roughly 8% compounded annual growth, through every type of market condition you can name.

The Math Most People Miss

Here is where the rate question gets interesting. Most people frame it as a binary: high rate equals bad time, low rate equals good time. The math tells a different story.

A $2.5M purchase with 25% down at 7% versus 6% works out to roughly a $1,250/month difference in payment, or about $15K per year.

Now apply San Carlos's historical appreciation to the same home. If rates drop to 6% next year and the market continues its historical trend, that same $2.5M home likely costs $150K to $200K more.

So the buyer who waits saves $15K on the rate side, then pays $185K more on the purchase side. The net cost of waiting is about $170K, every year you wait.

You are not saving money waiting for rates. You are paying for the privilege of watching the market move without you.

What 2026 Is Telling Us Right Now

The 2026 data only sharpens the point. Through May 2026, the average San Carlos single-family sale price has crossed $3M for the first time in history.

A few stats worth sitting with:

- 38% of all homes sold this year closed above $3M

- Homes in the $3M+ tier averaged just 18 days on market

- The $5M+ segment averaged $5.59M per sale

This is not a market sitting around waiting for rates to come down. Buyers are competing. Inventory is moving. The luxury tier is leading the charge.

A Note for Current Homeowners

The math above is framed around buyers, but if you are already a San Carlos homeowner thinking about upsizing or downsizing, the same principle holds, just from a different angle.

You are not sitting on the sidelines. Your existing equity is compounding with the market. Trading up means buying into appreciation on a larger asset, which historically has outperformed the cost of the larger mortgage. Trading down means harvesting equity that took years to build.

The framing changes, but the conclusion does not: waiting on rates is rarely the move that wins.

What Actually Wins in This Market

I have closed enough deals here to see the pattern clearly. The buyers winning in San Carlos are not the ones who timed it perfectly. They are the ones who committed to their horizon and bought the right home at the right price, without rushing into the wrong one.

Rate drops are a bonus. Appreciation is the strategy.

You cannot change the purchase price of your home after you buy it. But you can always refinance when rates come down. One of those is permanent. The other is temporary.

The Bottom Line

San Carlos has not punished buyers for buying in the last 15 years. It has punished people who waited. The data is clear, the trend is consistent, and the 2026 market is showing no signs of slowing.

If you are seriously considering a move, the question worth asking is not "What will rates do next year?" It is "Am I in the right home at the right price, for my horizon?"

That is a question the data alone can't answer for you. That is what working with the right agent is for.

Ready to Talk Strategy?

If you are thinking about buying or selling in San Carlos, the mid-peninsula, or anywhere in the Bay Area, I would love to walk through your specific situation. Every buyer's math is different, and the right move depends on your timeline, your finances, and the home that actually fits your life.

Reach out for a no-pressure conversation. We will look at the numbers together and figure out what makes sense for you.

Daniel Fridman

Fridman Homes / Ektra Real Estate